Lower Mortgage Rates Boost Your Buying Power: Here’s How

When mortgage rates decline, prospective homebuyers are presented with a golden opportunity to increase their purchasing power. Even a slight dip in interest rates can significantly impact your budget, allowing you to afford a larger home, lower your monthly payments, or secure better loan terms. If you’re in the market for a new home, understanding how lower mortgage rates can work in your favor is essential.

What is Buying Power?

Buying power refers to the amount of home you can afford based on your income, savings, and interest rates. When mortgage rates drop, you can afford a more expensive home without significantly increasing your monthly payment. This is because the interest portion of your payment is lower, so more of your money goes toward paying down the principal on your loan.

For example, if you were pre-approved for a $300,000 mortgage at 5% interest, a rate drop to 4% could mean you now afford a $315,000 home with the same monthly payment. This extra room can make a big difference in competitive housing markets, giving you access to better properties or neighborhoods.

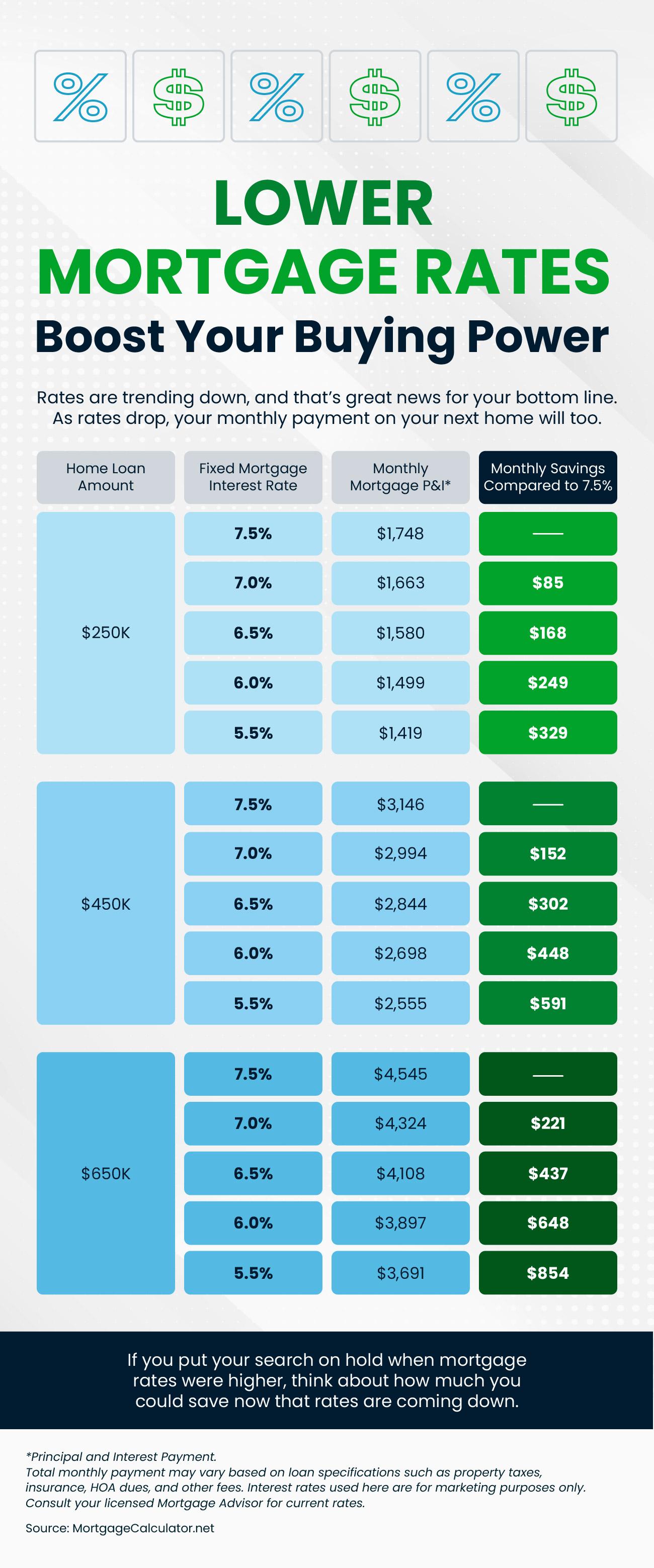

How Lower Rates Affect Monthly Payments

The primary way lower mortgage rates increase your buying power is through reduced monthly payments. When the interest rate is lower, a larger portion of each payment goes toward the principal rather than interest, helping you build equity in your home faster. This allows you to manage your budget more effectively, potentially making room for other expenses or investments.

For instance, if you take out a $250,000 mortgage for 30 years, at a 5% interest rate, your monthly payment (excluding taxes and insurance) would be around $1,342. If that rate drops to 4%, your payment would decrease to approximately $1,193—saving you nearly $150 per month. Over time, this savings adds up significantly.

Lower Rates Mean Better Loan Terms

Beyond higher affordability, lower mortgage rates may also lead to better loan terms. With lower rates, lenders may offer more favorable conditions, such as reduced fees or better options for down payments. This allows you to secure a more advantageous loan overall, minimizing the long-term costs of your mortgage.

Additionally, lower rates make it easier for existing homeowners to refinance their mortgages. Refinancing to a lower rate can result in substantial savings over the life of the loan, reducing both monthly payments and total interest paid.

BOTTOM LINE

In a climate of falling mortgage rates, homebuyers are in a stronger position to purchase the home of their dreams. Whether you’re a first-time buyer or looking to upgrade, taking advantage of lower interest rates can significantly boost your buying power, providing opportunities for savings and better terms. Now is an excellent time to explore the market and capitalize on these financial benefits. Let’s connect!

EN

EN

ES

ES